CF Benchmarks Newsletter - Issue 72

We spotlight what CME Group called its most successful crypto product launch ever, Bitcoin Friday futures; the granting of regulatory approval for options on BlackRock’s IBIT, and we offer our take on Bitwise's filing for a spot XRP ETF.

- CME Bitcoin Friday futures debut with record trade

- BlackRock's IBIT options set for OCC, CFTC approval

- Bitwise tables first US XRP ETF filing

Intact

The latest unexpected U.S. macro ‘diversion’, Friday's much stronger than expected U.S. September payrolls, finally put paid to remaining minority hopes of a 50 basis point cut at the Fed’s next meeting. But the absence of a mini market tantrum of the kind we’ve seen in recent months in reaction to both macro and policy outcomes was notable.

A hint earlier the same week by Fed chair Jerome Powell clearly hit the mark. He’d tentatively suggested “tension” between perceived employment weakening and objectively steady economic growth might be resolved by jobs data.

The stock market finished the week close to session highs, with 2-year and 10-year Treasury yields rising the most for weeks. Large cap crypto responded in line with its intermittent correlation to risk assets over the nearer horizon. Just a mild +2% for Bitcoin on the day though.

Rising Treasury yields were also a negative harbinger for 'yield steepening' trades that are tied to speculation of a more frantic pace of Fed easing.

All this suggests that, for now at least, the ‘base case’ projected by our research team in the inaugural report of their new Market Outlook series, would appear to be intact.

Go here to read CF Benchmarks’ “Market Outlook: Q4 2024: Recalibrating for the New Monetary Cycle”, or scroll down for a summary and excerpts.

To the extent the constructive scenario also indicates a benign outlook for digital asset prices, the pace of high-profile new initiatives by institutional product providers witnessed this year looks unlikely to abate for the time being.

In this edition alone, we spotlight what CME Group called its most successful crypto product launch, Bitcoin Friday futures; the granting of regulatory approval for options on BlackRock’s IBIT, while we note that Bitwise has ventured to file the first application for a U.S. ETF investing directly in XRP.

The backdrop includes resurgent Bitcoin ETF flows into the end of September after a moderate reversal, for a monthly positive total of $1.1bn, the best since July’s $1.2bn net inflow. That said, total flows from brand new ETH ETFs since launch have yet to eclipse the $2.95bn total outflow from Grayscale’s ETHE since it converted from an OTC fund at the same time.

On a ‘meta’ note, as well as showcasing our research team’s new quarterly outlook series, further down, we also spotlight our recently launched Weekly Index Highlights (WIH), and we outline how WIH, and our growing range of institutionally focused content can be integrated into and enhance existing cross-asset class monitoring.

CFB News

CME Bitcoin Friday Futures post record debut

The newest addition to CME Group's cryptocurrency product suite, Bitcoin Friday futures (BFF), the first weekly expiring futures contract of that range, launched at the end of last month.

Like all CME Group cryptocurrency products, BFF settles to CF Benchmarks' Bitcoin benchmark methodology.

With 31,000 contracts traded on the first day, including a block between Galaxy Digital and the digital assets arm of City of London-based broker, Marex, this was, by the numbers at least, CME's most successful crypto futures launch.

As previously outlined, at 1/50th of a Bitcoin, versus 5 BTC per regular contracts, BFF is the CME's smallest crypto contract, with specific benefits related to contract size alone:

- Smaller contracts should enable greater precision in sizing intended risk

- The same Bitcoin exposure as regular Bitcoin contracts, but with a lower upfront financial commitment

- Potential enhanced capital efficiency from margin savings over the shorter expiry; i.e., no outright margin costs, making BFF ideal for speculative short-term traders

- There are only ever 2 consecutive Friday-expiring BFF contracts listed at any one time, affording the choice of weekend exposure, if desired

Traders 'Large' and small

The impression that BFF is intended to expand the range of participants that can easily access the CME's regulated Bitcoin futures market beyond the CFTC designation of 'Large Trader', seems fair.

However, potential use cases are evident for institutional participants too, based on the fractional nature of BFF relative to larger CME BTC contracts, including Micro Bitcoin Futures (MBT), which equate to 1/10th of a Bitcoin each.

With BFF carrying costs minimised, due to weekly expiries, when positions are rolled forwards, basis should be more compressed over time in BFF trades compared to when exposure is sought via other CME BTC futures.

Broader benefits

Regardless of participant type though, BFF may also pose broader benefits as regards price discovery and market efficiency. Their greater capital efficiency and frequent expiries may enable – perhaps even incentivise – fine tuning of positions through more frequent transactions, leading to increased trading volume, and liquidity. In turn, this could attract an even wider base of participants.

BFF joins BRRNY club

Adjacent to potentially increased liquidity, a further plus pertains to the quality of liquidity available to BFF.

In a departure from other CME crypto products, BFF is the first that settles to our CME CF Bitcoin Reference Rate - New York Variant (BRRNY).

BRRNY is among our growing range of reference rates synchronised with the traditional U.S. market close at 4 PM New York Time, vs. the 4 PM London Time referenced by the CME CF Bitcoin Reference Rate (BRR).

BFF can therefore be placed alongside the growing raft of assets referencing BRRNY; chiefly including the brace of U.S. Bitcoin ETFs that launched in January which we dubbed the 'BRNNY Six' - the Top Six by assets under management.

Evolving liquidity

Whilst wider access to regulated Bitcoin trading, and the reduced financial commitment indicated by BFF are an important milestone, this first CME crypto contract to settle to the BRR's New York variant also represents an evolution of 'The BRR Liquidity Complex'.

This evolution will be confirmed over time, but the seismic influx of fund assets referencing BRRNY suggests a new 'centre of gravity' for the liquidity complex that can benefit all products within it, now including BFF.

IBIT Options move a step closer

With BlackRock's iShares Bitcoin Trust ETF (IBIT) now the largest spot Bitcoin ETF (net assets were pushing $23bn at the time of writing), the SEC's approval, late last month, of options trading on the largest product referencing BRRNY helps pave the way for a further significant enhancement of the BRR Liquidity Complex effects we outlined above.

It's worth noting though, that unlike the SEC, the two bodies that need to provide the final leg of approval for IBIT options – The Options Clearing Corporation (OCC) and the CFTC – do not follow any specific guidelines on the length of their determinations.

Still, the SEC's uncharacteristically swift completion (for a crypto product) via an Order Granting Accelerated Approval, and its uncontroversial commentary, tend to indicate a relatively prompt clearing and commodities sign off.

The SEC's observations suggest it was satisfied with the liquidity of the underlying stock, Nasdaq's surveillance arrangements, and other points that might potentially have posed concerns.

The exchange's setting of what the the SEC called "the lowest position limit available in the options industry", undoubtedly helped. The limit, set at 25,000 IBIT options contracts, is (according to the SEC) "extremely conservative and more than appropriate given the IBIT’s market capitalization, average daily volume, and high number of outstanding shares." There were over 600 million shares outstanding as of August 12th.

Further options

Based on the above, speculation of further incoming option chains on U.S. spot Bitcoin ETFs – including other BRRNY Six funds – isn't unreasonable.

Likewise, Nasdaq's pending separate application, filed in August, to list options settling directly to BRRNY, should in theory be approaching the front of the queue.

Meanwhile, although the spot Ether ETFs that came to U.S. markets more recently have experienced more modest flows and volumes than the Bitcoin funds, activity and liquidity in the fastest growing Ether funds is well within the bounds of instruments that have generally been granted regulatory clearance for options trading.

Chiefly, inflows into BlackRock's iShares Ethereum Trust ETF (ETHA), which is underpinned by the ETHUSD_NY, benchmark, have risen to around $1bn since its late-July listing.

BlackRock and Nasdaq filed an application to list ETHA options in August.

Bitwise's XRP ETF filing pushes the envelope

The investment firm's application landed the same day as the SEC's Ripple appeal

Bitwise Asset Management is the first U.S. institution to put its head above the parapet with a filing for a spot fund investing in the digital asset that's, arguably, evidenced the most high profile regulatory controversy in recent years.

The group announced, on October 2nd, its S-1 (initial registration statement) filing to the SEC of Bitwise XRP ETP, which will invest in the token directly.

The crypto focused investment firm already manages one of the most successful spot BTC ETFs in terms of AuM, Bitwise Bitcoin ETF (BITB). As well, it's Bitwise Ethereum ETF (ETHW) now ranks third by AuM, following it's July launch.

Just as exciting for CF Benchmarks, of course, is that Bitwise has once again opted to deploy one of our regulated benchmarks, the CME CF Ripple-Dollar Reference Rate - New York Variant (XRPUSD_NY), to calculate the NAV of its XRP fund.

The group utilises our Bitcoin and Ether benchmarks, BRRNY and ETHUSD_NY, to strike NAV for BITB and ETHW.

The Long View

Given the widely aired Ripple controversy, and uncertainty over its complete resolution, Bitwise's XRP ETF filing clearly has an eye to the medium term, at least, as regards expected progress towards regulatory approval.

Amid tentative hopes that Ripple Labs might soon put its history of legal contention with the SEC behind it, the controversy was reignited last week when the Commission followed through on a long speculated appeal.

It follows an order by a federal judge in August that Ripple Labs pay a fine of just $125m for violation of securities laws in relation to institutional sales of XRP. The SEC had sought a penalty closer to £2bn. Disgorgement was not part of the penalty.

Around a year earlier, the same judge had issued a partial ruling to the effect that programmatic sales of XRP to retail exchanges did not violate securities laws.

The SEC filed a notice of appeal against the August ruling on October 2nd, the same day Bitwise announced its filing, and days before the SEC's right of appeal was set to expire on, October 7th.

The Commodity Condition

Around the time when U.S. Ether ETFs received regulatory approval, we noted the process strongly supported our long-held view that a CFTC regulated commodity futures market in a digital asset is among the critical conditions that needs to be satisfied for an exchange traded product investing in that asset to be approved. (For clarity, this is an evidence-based opinion only).

CF Benchmarks's long-established partnership with CME Group resulted in the launch of our CME CF Ripple-Dollar Reference Rate (XRPUSD_RR) in July. XRPUSD_RR is published daily at 4 PM London Time.

The XRPUSD_NY variant, which was launched in September, is published at 4 PM New York Time.

The CME's longstanding playbook for making cryptocurrency derivatives available for trade is to first jointly launch a regulated reference rate with CF Benchmarks.

As observed in the cases of CME's Bitcoin and Ether derivatives, its crypto futures and options markets are generally launched some years after the inception of the reference rates. There is, as yet, no CME XRP futures market.

Looking forward

As for the SEC's resumed litigation, various timelines have been speculated.

Still, assuming simplified due process, the Commission's appeal, filed to the U.S. Court of Appeals for the Second Circuit, is only likely to begin moving through the court towards the end of this year.

Meanwhile, the outcome of U.S. Elections in November could impact how the SEC's continuing prosecution unfolds, particularly if a new administration results in a change of leadership at the SEC.

Even if so, that event could still be several months away.

Markets

Introducing the CF Benchmarks Market Outlook

As noted earlier, in their inaugural Market Outlook: Q4 2024 - Recalibrating for the New Monetary Cycle, the CF Benchmarks research team, led by Gabriel Selby, CFA and Mark Pilipczuk, identified a 'Base Case' of stabilising global growth, amid "materially lower" recession probabilities as the one most likely to prevail over the quarter.

Highlights

- As the analysts state in the section of their report covering Consensus Forecasts, the outlook for risky assets (with similar, if not identical, implications, for digital assets) includes stocks continuing to grind higher into the end of the year, amid robust EPS growth and easing PE ratios.

- Among Secular Themes for crypto assets that can loop back to returns, the team spotlights a focus on Scalability, that could leave Ethereum as the "preferred choice for developers and end users, due to its robust, interoperable ecosystem and large user base."

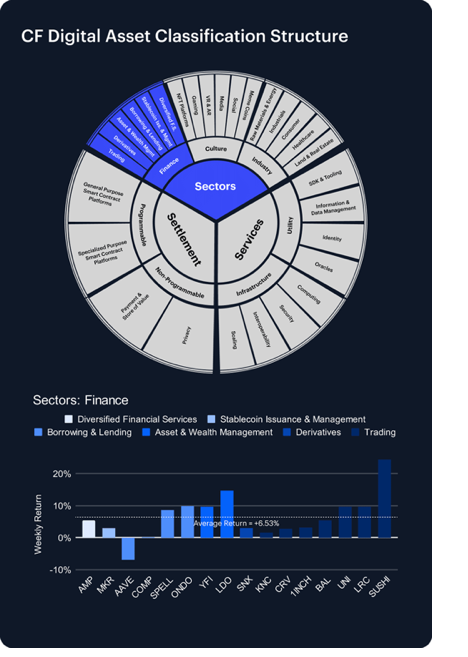

- The research team also include a section on the currently hot topic of stablecoins, titled 'Stablecoin Use to Rise Further'. There, they forecast that transaction volume will continue to increase under all scenarios, as shown in the excerpted image below.

Additional sections cover topics like the accelerating pace of institutional tokenisation of real-world assets; the complement of, and potential competitor to traditional cloud computing represented by Decentralized Physical Infrastructure Networks (DePINs), and much more.

Head to the Market Outlook: Q4 2024 page for more details

Click here to download the complete report

Featured content: Weekly Index Highlights

Five reasons to catch Weekly Index Highlights every Monday

Our Weekly Index Highlights series is designed to provide quick insights into crypto market events of the past week. Here’s a detailed look at what they offer.

CF Benchmarks’ Weekly Index Highlights, our series of concise crypto market summaries, has now been running for around a month.

Many market professionals have already discovered the benefits of having a trustworthy go-to source of unbiased commentary to hand every Monday, to quickly get up to speed with how digital assets fared the previous week.

And because their cadence is weekly, the highlights are easy to integrate into analyses of the broader market context institutional participants typically keep abreast of already.

Naturally, these weekly reports showcase CF Benchmarks’ high-integrity rules-based methodology; spanning single asset indices covering Bitcoin, Ethereum, Solana, Ripple and other large caps (the CME CF Single Asset Series); portfolios measuring whole market beta (the CF Capitalization Series); and indices focused more specifically on blockchain thematics (the CF Classification Series).

All told, our Weekly Index Highlights (WIH) are the only high frequency, quickly digestible read on cryptocurrency markets from a regulated Benchmark Administrator.

Weekly Index Highlights: A Closer Look

It's also worth noting Weekly Index Highlights are an integral part of CF Benchmarks’ complete research and content portfolio.

Our product, research and content teams have established a broad suite of publications, with each intended to supplement to the sum of the parts.

This enables a credible and comprehensive view of the investible digital asset market.

Below, we spotlight 5 key ways Weekly Index Highlights integrate into CF Benchmarks' broader suite of research content, providing an invaluable addition to any market monitoring routine.

- An impartial weekly view of the crypto market. As the first ever crypto Benchmark Administrator, regulated under UK and EU Benchmarks Regulation frameworks, CF Benchmarks’ market integrity is guaranteed by obligation. Meanwhile, the deep expertise of our practitioners in defining and measuring crypto prices, means our takes are second to none – but with no axe to grind.

- Lift the lid on Bitcoin’s credit market. We bring our track record of devising, publishing and administering the most institutionally trusted pricing sources to bear in calculation of the CF Bitcoin Interest Rate Curve (CF BIRC). This ensures all points on the curve are representative, replicable and resistant to manipulation. In turn, it means CF BIRC is the only curve that can meet the stringent standards institutional Bitcoin borrowers and lenders are subject to. WIH shows how these rates are moving over the short term.

- The only true measure of CME Bitcoin implied volatility. The CF Bitcoin Volatility Index Settlement Rate (BVXS) measures the implied volatility of the CME Bitcoin Options market, 30 days forwards. This makes BVXS the most accurate gauge of implied volatility in the primary Bitcoin options market that major institutions transact in. Weekly Index Highlights offer an invaluable view of implied volatility's impact on the BTC spot market.

- A sneak peek at quarterly crypto drivers. Weekly Index Highlights include an animation of the CF Digital Asset Classification Structure (CF DACS), our unique digital asset taxonomy that delineates the investible crypto universe. CF DACS is increasingly used by institutional investors to demarcate the precise blockchain economic factors driving a portfolio, or the entire digital asset market. CF DACS animations enable an instant grasp of how these drivers are evolving. CF DACS is also an integral part of CF Benchmarks Quarterly Attribution Reports (QAR). Each QAR decomposes prevailing blockchain economic themes by determining the precise contribution of each CF DACS element on portfolio index returns.

- A snapshot of ETH staking rewards. Our research team commented on a surge in Ethereum network fees in their September Market Recap, observing that total fees jumped 89% month-on-month. That stands alongside the CF ETH Staking Reward Rate (ETH_SRR) summary in our September 30th Weekly Index Highlights; down -11.25% on the week, and -9.99 YTD. Collating the fee surge with ETH_SRR’s weekly collapse raises important questions. Like, whether ballooning fees incentivised increased validator participation, thinning out rates. It's an open question. But it does illustrate how each weekly sketch on ETH_SRR provides a valuable nugget of additional context.

Read all Weekly Index Highlights here.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.